There are basic but fundamental errors at the heart of the Wolf-Pettis thesis. Most importantly, there is a misunderstanding of the meaning and definition of 'saving'. 1/

24.06.2025 13:30 — 👍 98 🔁 25 💬 6 📌 6There are basic but fundamental errors at the heart of the Wolf-Pettis thesis. Most importantly, there is a misunderstanding of the meaning and definition of 'saving'. 1/

24.06.2025 13:30 — 👍 98 🔁 25 💬 6 📌 6Another great thread from Glenn, who deserves more followers here IMO. He has been doing yeomen’s work dispelling this kind of nonsense in detail. carnegieendowment.org/posts/2009/1...

14.12.2024 16:59 — 👍 28 🔁 7 💬 1 📌 0

In aggregate, 3.4B passengers a year translates into ~45 terawatt-hours (TWh) per year.

In '24, China will consume around ~10,000 TWh.

So this is equivalent to ~0.5% of total power consumption in China a year.

This compares with est. ~78 TWh for the entire light NEV fleet.

One under-appreciated energy efficiency advantage of HSR vs. EVs is higher effective seat-yield: HSR in China is typically ~80% seat-yield vs. <1/3rd for passenger cars.

A fully packed EV can be nearly as efficient as HSR but cars are most often used by a single person/driver.

This compares to ~210 watt-hours per km for a typical electric vehicle.

An EV with two passengers would be ~105 watt-hours per px-km.

HSR can transport passengers at an avg. electricity cost of ~38 watt-hours per px-km.

The typical ~348 km trip takes up ~13.2 kWh, or around half a days worth of typical power consumption.

The total build cost for ~45,000 km was ~$1T, or ~$24M per km.

Amortized across 124B passenger rides comes out to $8 per ride and 2.3 cents per km.

Avg. mfg. wage is ~$8/hour today, so the amortized upfront build cost per ride is about 1 hour's worth of avg. mfg. work today.

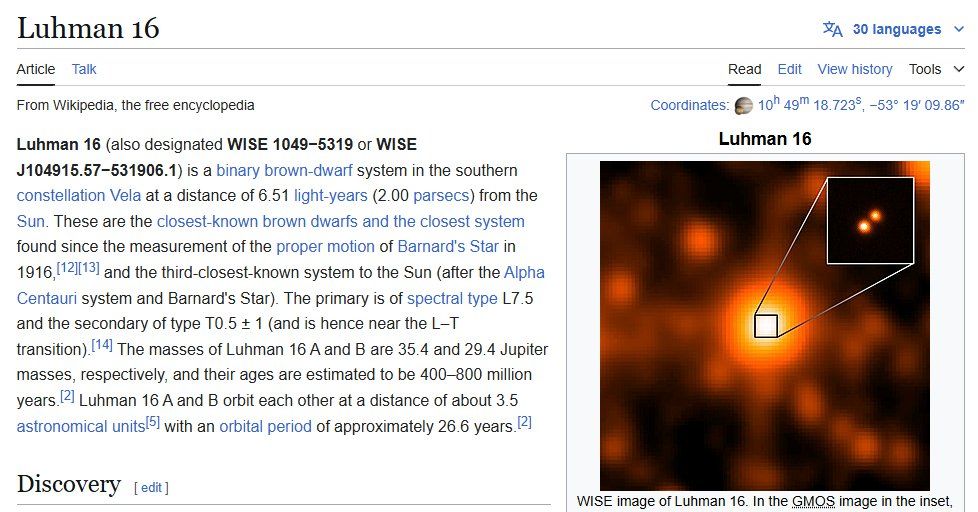

If the HSR network were frozen today at current run-rate of ~3.4B px/year for the next 30 years, this would aggregate to 124B passengers traveling ~43T kilometers, or ~7.1 light years.

This gets you to Luhman 16, the third-closest known star.

Since 2009, China's HSR network has served ~22 billion passengers traveling an aggregate ~7.6 trillion kilometers (~348 km/trip).

This is equivalent to ~26k round trips to the sun, or ~0.80 light years.

I am not that familiar with it but it seems promising.

11.12.2024 20:17 — 👍 1 🔁 0 💬 0 📌 0

There really is much to be optimistic about in the future for our kids and grandkids.

We just have to get their in one piece so we can deliver it to them.

And I should emphasize that this should not just be about 🇺🇸+ 🇨🇳 but everyone on the planet.

Where this ends up is a much harder question to resolve but as long as people don't get so emotional and nasty about it, I am confident we will be able to collectively figure it out.

🇺🇸+ 🇨🇳 will continue to drift apart economically and that's perfectly fine! (again, as long as it is done peacefully)

The world will need to find a new equilibrium point — and new (or modified) organizational structures.

Thus 🇺🇸-🇨🇳 trade & tech war is simply the manifestation of the underlying reality that 🇺🇸 + 🇨🇳 are drifting apart in terms of economic compatibility.

Levelheaded recognition of this reality (i.e. not freaking out about it) is key to managing a peaceful transition.

Why dedicate this increasingly scarce pool on meeting foreign demand when there is still work left to be done at home?

11.12.2024 19:48 — 👍 1 🔁 0 💬 1 📌 0

Meanwhile, China is increasingly less thrilled about being valued only for its labor.

Its blue-collar labor pool is shrinking and becoming more of a precious commodity and wages rising, commensurately.

Within this framework, 🇺🇸 has responded rather predictably by effectively restricting or banning imports of everything ranging from Tiktok to Huawei smartphones to BYD cars.

While various reasons are given (reciprocity, blanket "national security"), economic competition is really at the heart of it.

🇺🇸+ 🇨🇳 are becoming less economically compatible over time.

Understandably, 🇺🇸 did not want to give up the economic "high ground" that powered a comfortable life for the vast majority of citizens.

Also understandably, 🇨🇳 wanted to bring such a life to its billion-plus citizens.

Ultimately, what has really changed the equilibrium was China quite rapidly moving up the value chain (faster than most expected) and starting to develop higher-value tech/IP/brand-driven products that were competing with U.S. brands and MNCs.

11.12.2024 19:48 — 👍 1 🔁 1 💬 1 📌 0This trading relationship dominated over two decades from the mid-90s when China first started emerging as a major manufacturing destination to the mid/late-2010s when the current trade war started to brew.

11.12.2024 19:48 — 👍 0 🔁 0 💬 1 📌 0

This reciprocal trade relationship was fundamentally based on the respective strengths & weaknesses of both sides.

China had a large, productive and inexpensive labor pool.

The U.S. had the largest modern consumer market, leading technology and advanced human capital.

The U.S.-China trade relationship of the first part of the 21st century was at its core predicated on 🇺🇸 retaining brand/tech/IP value and outsourcing production to 🇨🇳 mfg. partners.

In return, 🇨🇳 opened up its domestic market to these high-value 🇺🇸 products.

The mistakes came from poor strategic & tactical decisions on whether or not to re-invest windfall profits back into the business, in an attempt to get ahead of new technologies like electrification that could disrupt existing business models.

09.12.2024 14:44 — 👍 1 🔁 0 💬 0 📌 0

There are lessons to be learned here.

The lesson isn't that GM should have never entered China.

It earned tens of billions of incremental dollars for doing almost no work and putting very little capital at risk.

Its Chinese competitors did, including its JV partner SAIC.

And once EV technology came of age, the writing was on the wall in China. It was only a matter of time.

It decided to mostly distribute to shareholders through dividends, debt paydowns and buybacks.

Where it did reinvest back into the business, with the benefit of hindsight, we now know it did not do it particularly well or efficiently.

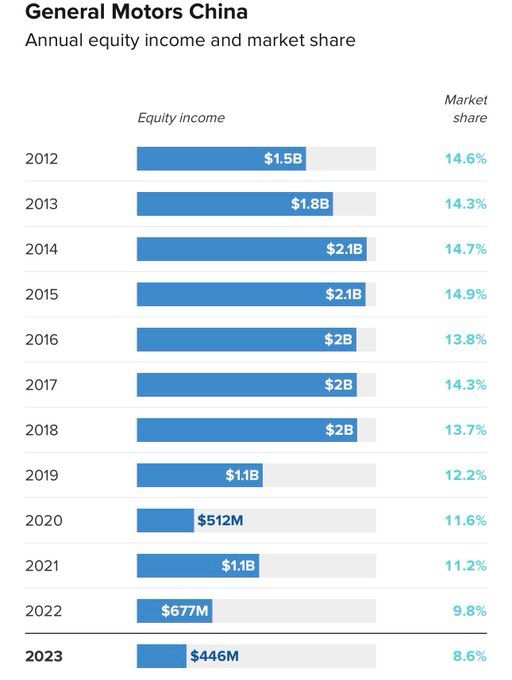

GM China provided a lifeboat for GM when it underwent restructuring during the GFC.

For a period of time, GM China generated more net earnings for GM shareholders than the rest of the business combined.

These charges are the official recognition of what's been known for a few years by now: After nearly three decades, GM won't be selling that many cars in China anymore.

Off its initial investment of <$1B, it made $17B ($22B minus $5B in charges).

At least a 17x return. Not too shabby.

The writedown is a non-cash charge and the restructuring costs are presumably going to be covered by ongoing sales as the operations wind down.

The $5B represents cumulative equity income from around mid-2018 to today.

Last week, GM announced that it was going to be taking $5B in charges on its China joint ventures, split between a writedown of $2.7B on its China JVs + another $2.6-2.9B in retructuring charges related to "plant closures and portfolio optimization".

www.reuters.com/business/aut...