Did you know that most of the equity risk premium is realized on macro announcement days? I discuss the latest research on this topic and test a simple strategy around nonfarm payrolls.

www.quantseeker.com/p/weekly-res...

@quantseeker.bsky.social

Quant investing and trading. Research and trading strategies. For information and education only, not investment advice. Weekly Newsletter: https://www.quantseeker.com/

Did you know that most of the equity risk premium is realized on macro announcement days? I discuss the latest research on this topic and test a simple strategy around nonfarm payrolls.

www.quantseeker.com/p/weekly-res...

A fresh roundup of the latest investing research is out.

➢ Predicting Crypto Using Sentiment

➢ A Strategy Based on FX Mispricings

➢ Option-Based Return Predictors

➢ A Regime-Switching Model

➢ ...and much more.

👉 Join 5,000+ investors and quants:

www.quantseeker.com/p/weekly-res...

This just arrived. Looks like a great read.

25.05.2025 19:57 — 👍 0 🔁 0 💬 0 📌 0

A fresh roundup of the latest investing research is out.

➢ Macro Announcement Risk Premia

➢ A Mean-Reversion Strategy

➢ Complex or Simple Models?

➢ Diversifying with Listed Real Estate

➢ Great Blogs, Repositories, and Podcasts

➢ ...and much more.

www.quantseeker.com/p/weekly-res...

New article by Antti Ilmanen on understanding expected returns. Always a must-read.

www.aqr.com/Insights/Res...

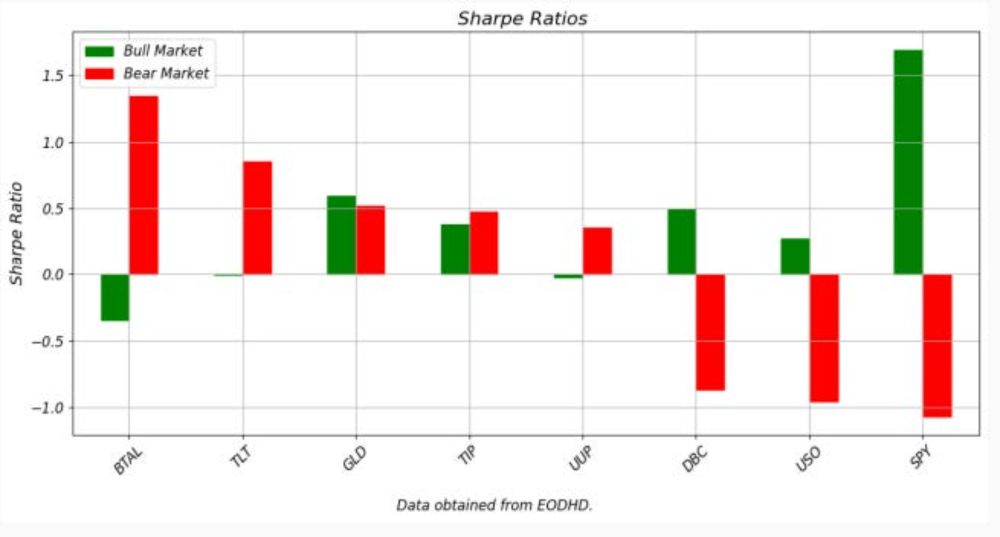

A new article is out where I explore which assets and strategies tend to perform well during bear markets.

www.quantseeker.com/p/what-works...

A fresh roundup of the latest investing research is out.

Some of the topics covered:

➢ Bond Return Predictability

➢ Timing Momentum

➢ Stock Return Predictability

➢ Disagreement in Option Markets

➢ Great blogs, repositories, and podcasts

➢ ...and much more

www.quantseeker.com/p/weekly-res...

A new roundup of the latest investing research is out.

➢ Sector Exposure in Commodity Signals

➢ Earnings and Price Momentum

➢ Sector Allocation with LLMs

➢ Macro News Attention

➢ ...

Read more here:

www.quantseeker.com/p/weekly-res...

A new roundup of the latest research on investing is out.

➢ Currency Anomalies

➢ Improving Momentum Strategies

➢ Finance Applications of LLMs

➢ Volatility Forecasting

➢ Great blogs, repositories, and podcasts

➢ ...

www.quantseeker.com/p/weekly-res...

In my new post, I discuss research on:

- Economic Uncertainty and Expected Returns

- Emerging Market Debt

- Predicting Overnight Returns

www.quantseeker.com/p/weekly-res...

A new roundup of the latest investing research is out.

Topics:

➢ X-Asset Momentum

➢ Political Risk and Return Predictability

➢ LLMs and News Sentiment Trading

➢ Great blogs and podcasts

➢ ...

www.quantseeker.com/p/weekly-res...

New blog post: I explore how the slope of the VIX term structure can be used to time volatility exposure, reviewing key research and testing some trading signals.

www.quantseeker.com/p/timing-vol...

In my new blog post, I discuss research on:

- Properties of Drawdowns

- News-Driven Commodity Trading

- Extracting Alpha from Crowding

www.quantseeker.com/p/weekly-res...

A new roundup of the latest research on investing is out.

Topics:

➢ Overnight Stock Returns

➢ Factor Exposures and Quantile Regressions

➢ Asset Allocation and Macro Regimes

➢ Great blogs, repos, podcasts

➢ ...

www.quantseeker.com/p/weekly-res...

Three great books.

14.03.2025 09:55 — 👍 1 🔁 0 💬 0 📌 0

A new blog post is out where I explore short-term mean reversion signals.

www.quantseeker.com/p/short-term...

In my new post, I discuss research on:

Generating Alpha from Analysts

Protecting Against Inflation

Profiting from Macro Announcements

www.quantseeker.com/p/weekly-res...

A new roundup of the latest research on investing is out.

Topics Covered:

➢ Predicting Commodity Returns

➢ Restoring the Value Premium

➢ ETF Momentum

➢ Great blogs, repositories, and podcasts

➢ ...

Join fellow investors:

www.quantseeker.com/p/weekly-rec...

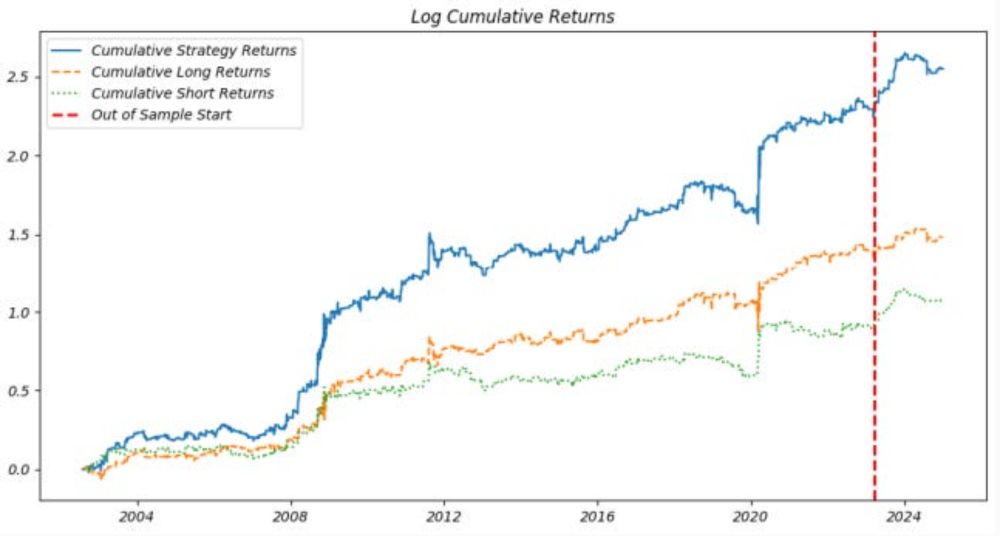

New Article: The pre-FOMC announcement drift isn’t dead, it’s alive and well. I review the research and test the strategy using data through 2024.

www.quantseeker.com/p/trading-th...

A new blog post is out: I discuss and test a short-term mean reversion signal between stocks and bonds.

www.quantseeker.com/p/exploiting...

A new roundup of the latest research on investing is out.

Topics:

➢ Tail risk in oil markets

➢ Extracting sentiment with FinGPT

➢ The impact of gamma on volatility

➢ Portfolio construction

➢ Great blogs, repositories, and podcasts

➢ ...

www.quantseeker.com/p/weekly-rec...

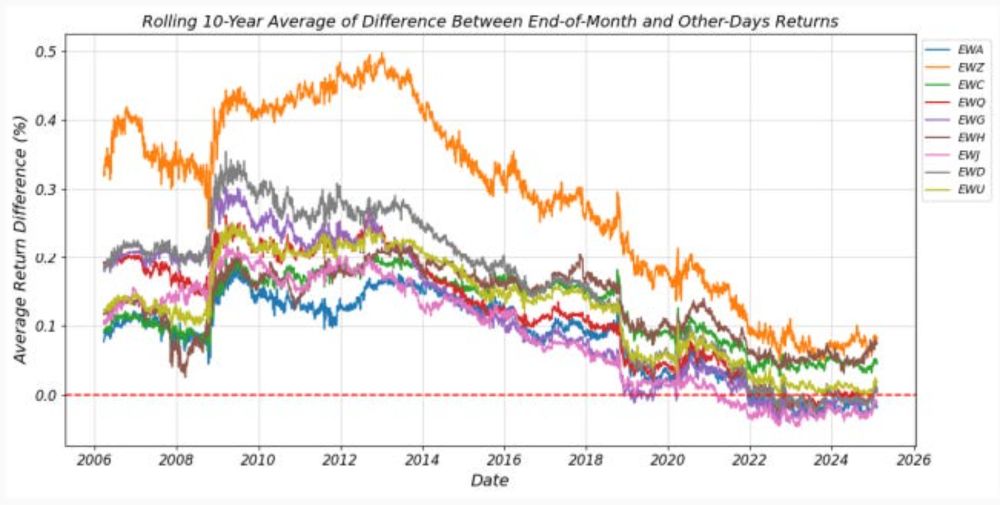

New blog post: Turn-of-the-Month Strategies: Do They Still Work?

I explore key academic findings and test strategies across a range of ETFs. Are the returns still there?

www.quantseeker.com/p/turn-of-th...

A new recap of the latest research on investing is out.

Topics Covered:

➢ Alpha in Premier League Betting

➢ Crypto

➢ Value Investing

➢ Seasonalities in Option Returns

➢ Large Language Models

➢ ...and much more

Read and join the community:

www.quantseeker.com/p/weekly-rec...

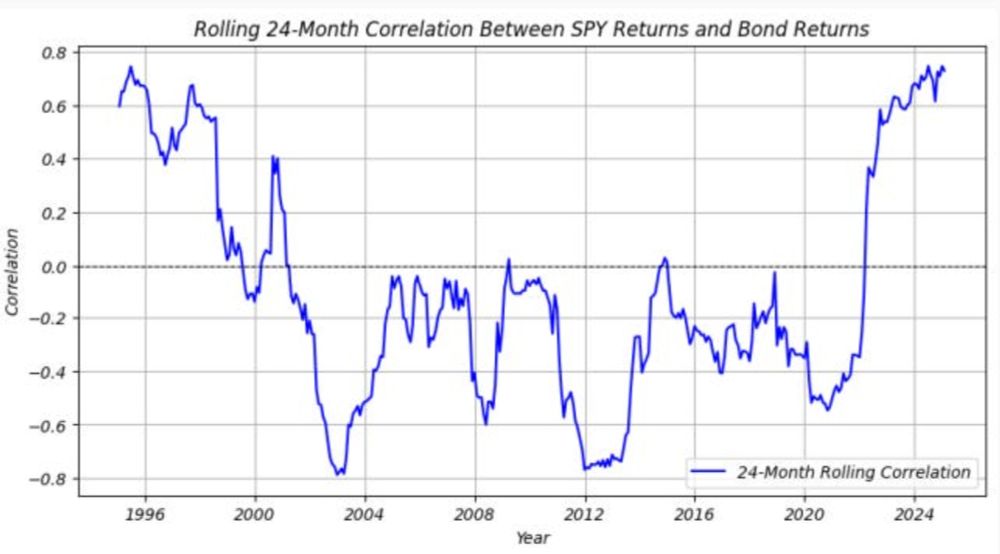

The stock-bond correlation plays a crucial role in portfolio construction, risk management, and asset allocation. In my latest article, I explore its significant time variation, the economic forces that drive it, and the practical implications for investors.

www.quantseeker.com/p/exploring-...

A new recap of the latest research on investing is out!

Read and join the community:

www.quantseeker.com/p/weekly-rec...

A new edition of my weekly roundup of the latest research on investing is out!

Read and join the community:

www.quantseeker.com/p/weekly-rec...

New blog post: While trend and breakout signals are popular in crypto markets, recent research suggests alternative signals beyond momentum. I test two such signals and their combination with momentum.

www.quantseeker.com/p/beyond-mom...

A fresh recap of the latest research on investing is out!

www.quantseeker.com/p/weekly-rec...

This new paper studies portfolio protection strategies, highlighting the need for diversification. It proposes a mix: 40% SPX rolling puts, 20% Trend, 20% Long Rates Vol, and 20% Quality, to manage the diverse intensity and length of equity drawdowns.

Read paper here: papers.ssrn.com/sol3/papers....

Can industry momentum strategies be enhanced with news sentiment and dispersion? I explore how these factors can improve traditional momentum strategies, finding significant performance gains, especially at more granular industry levels.

www.quantseeker.com/p/improving-...