In making this course, I've borrowed a lot of material from other teachers. Thanks to all of you who makes your teaching material publicly available!

04.06.2025 13:31 — 👍 1 🔁 0 💬 0 📌 0

I also have quite a few exam questions and problem sets to share to anyone who wants to teach similar material. Just email me if you want them.

04.06.2025 13:31 — 👍 1 🔁 0 💬 1 📌 0

The course covers business-cycle frameworks (RBC and NK), Frictional Labor Markets (McCall, Burdett-Mortensen, DMP) and consumption-savings dynamics with incomplete asset markets (both partial and general equilibrium).

04.06.2025 13:31 — 👍 0 🔁 0 💬 1 📌 0

GitHub - erikoberg/teaching_material

Contribute to erikoberg/teaching_material development by creating an account on GitHub.

For several years, I've been teaching Ph.D. Macroeconomics II in the first-year Ph.D. course sequence here in Uppsala. I've uploaded all lecture notes in the attached link, in case this is to the interest of someone else.

github.com/erikoberg/te...

04.06.2025 13:31 — 👍 4 🔁 0 💬 1 📌 0

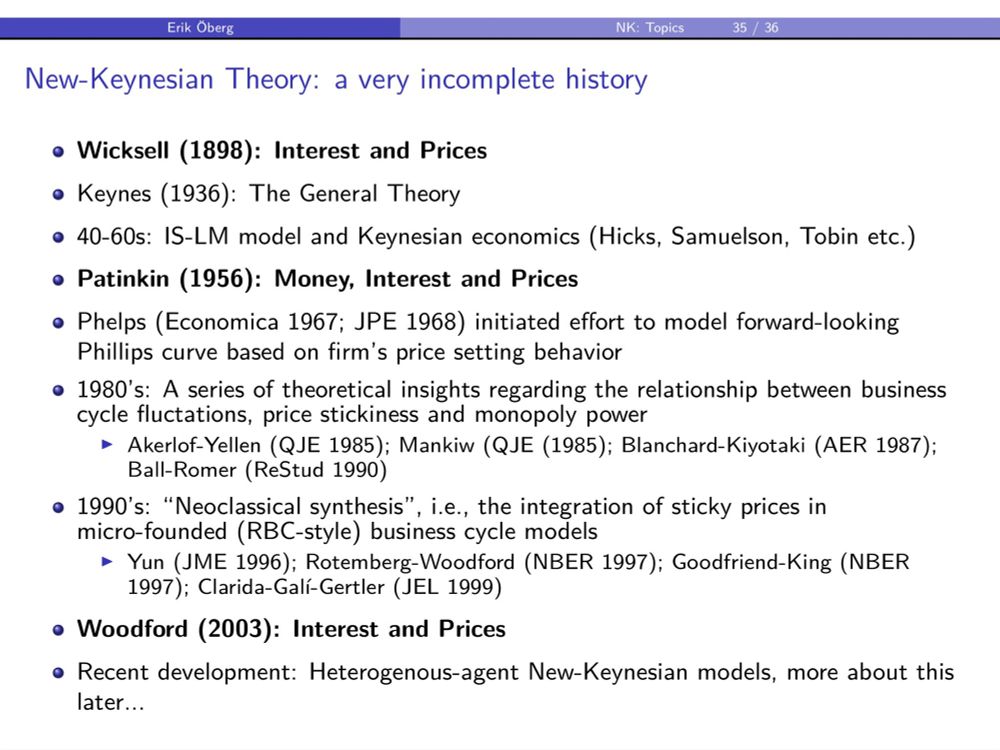

Fair one-slide summary of literature leading up to 3-equation New-Keynesian model?

20.03.2025 08:02 — 👍 2 🔁 0 💬 0 📌 0

Nationalekonomi som ingenjörsvetenskap? Ett förslag till ett nytt utbildningsprogram – Nationalekonomiska Föreningen

Skriver i senaste @ekonomiskdebatt.bsky.social om "Nationalekonomi som ingenjörsvetenskap? Ett förslag till ett nytt utbildningsprogram". Samlar upp en del tankar och diskussioner som förts med kollegor och här på sociala medier.

nationalekonomi.se/artikel/nati...

14.03.2025 09:23 — 👍 6 🔁 1 💬 0 📌 0

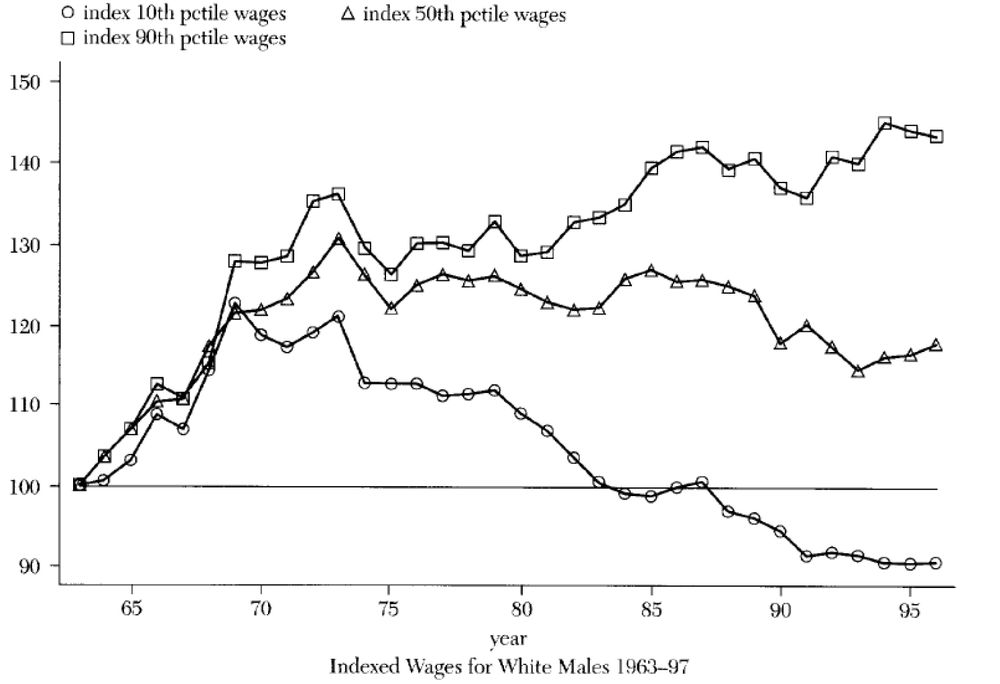

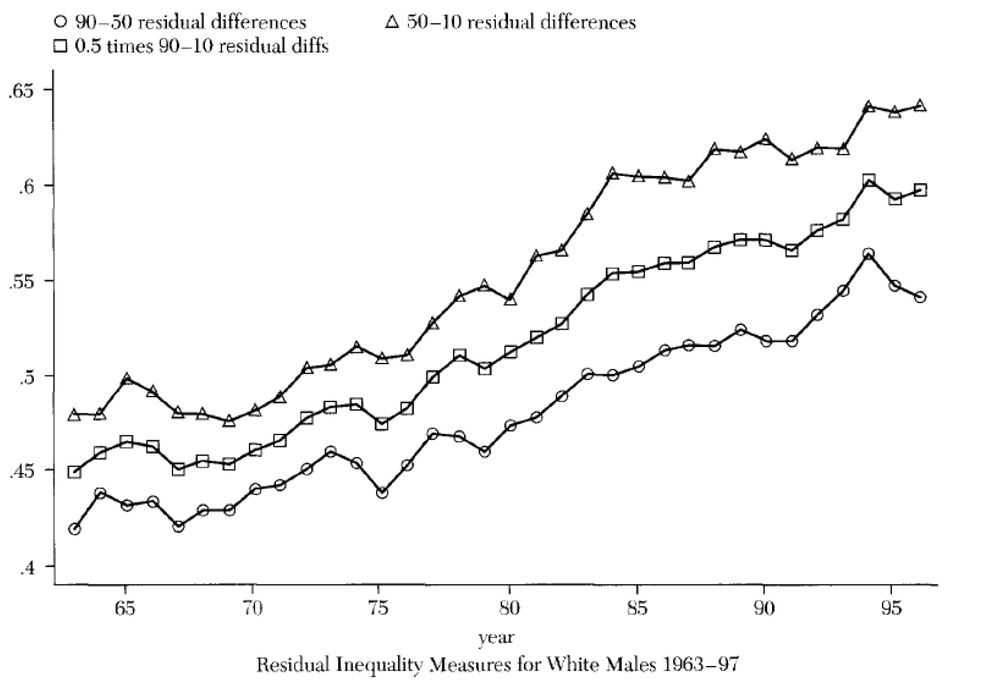

Does anybody know if there exist an updated version of these graphs from Acemoglu (JEL 2002) somewhere?

I'm preparing lectures on search models and wage dispersion, in which I use these graphs to introduce the concept of residual wage dispersion, but they are a bit outdated.

11.03.2025 09:49 — 👍 0 🔁 0 💬 2 📌 0

This is very helpful - thx a lot!

31.01.2025 11:53 — 👍 1 🔁 0 💬 0 📌 0

Yes, numerous measurement issues. I was thinking about how to start exploring this. I learnt today that there were some nice efforts in the 90's to clean "Solow residuals" from labor utilization (exploiting some optimality conditions and firm data on other firm inputs). E.g. Basu-Kimball (1997)

30.01.2025 13:45 — 👍 0 🔁 0 💬 0 📌 0

Econ Question: How much of fluctuations in TFP can be accounted for by fluctuations in worker effort? Like in booms, firms use the hours worked available to them more efficiently. Is there any attempt out there to answer this of related questions?

30.01.2025 09:27 — 👍 1 🔁 0 💬 2 📌 0

She has several other interesting papers and projects too, e.g., about in-house hiring vs staffing agencies, misallocation across firms and wealth inequality. See her webpage for more.

sites.google.com/view/agnetab...

27.01.2025 13:32 — 👍 1 🔁 0 💬 0 📌 0

Very happy to share that @agnetaberge.bsky.social will join

Uppsala as a post-doc in the fall! Agneta is macroeconomist coming out of IIES with a focus on labor markets and wage setting. In her JMP, she develops a theory of two-tier collective wage bargaining.

drive.google.com/file/d/1x-tV...

27.01.2025 13:32 — 👍 11 🔁 0 💬 1 📌 1

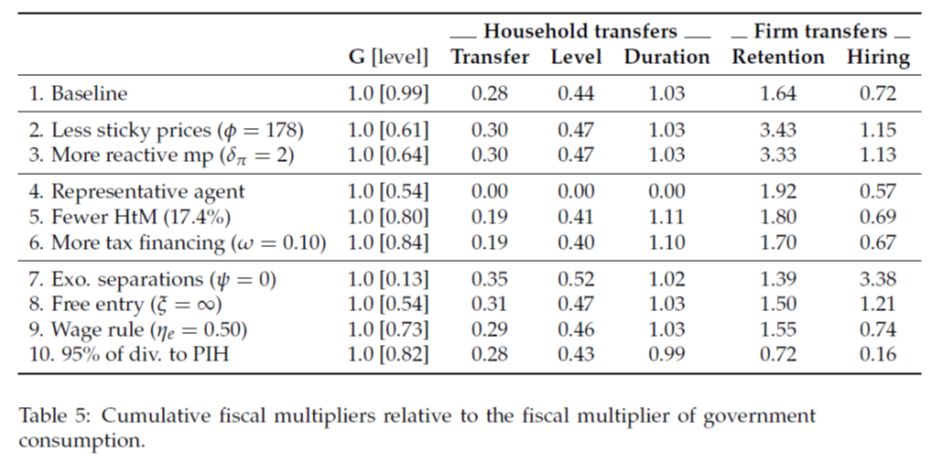

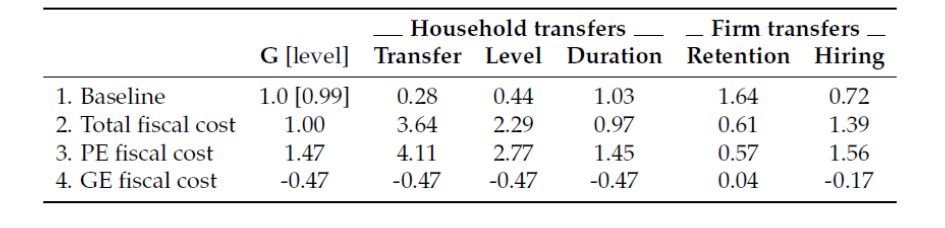

Table heading missing. The table shows fiscal multipliers and fiscal cost normalized with the counterpart numbers from a pure government spending shock.

16.01.2025 10:19 — 👍 0 🔁 0 💬 0 📌 0

Two closely related papers are Wolf (2024) and Ferriere-Navarro (2024). Be sure to check them out.

economics.mit.edu/sites/defaul...

axelleferriere.github.io/files/FN_IMF...

16.01.2025 09:58 — 👍 0 🔁 0 💬 0 📌 0

We also identify some key parameters/moments that do make a difference for these conclusions. One of them is the marginal propensity to consume out of profit income, for which we need more evidence. In our view, these findings paint an agenda for future research.

16.01.2025 09:58 — 👍 0 🔁 0 💬 1 📌 0

Importantly, these conclusions are insensitive to changes to a big part of the model parameter space, as per the reasoning above. For details about this, see the paper.

16.01.2025 09:58 — 👍 1 🔁 0 💬 1 📌 0

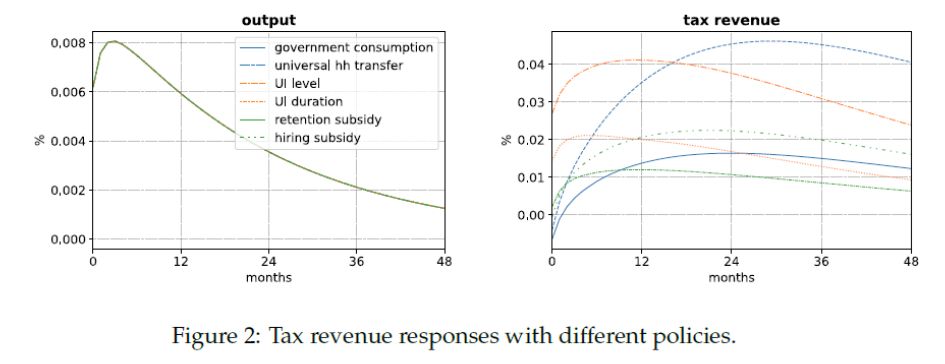

This feature gives a double dividend: saving a job is cheap relative to creating to new one. Moreover, saving a job avoids vacancy-depletion effects (as in Coles-Kelishomi (2018)), and reduces the unemployment risk that households face a lot.

16.01.2025 09:58 — 👍 1 🔁 0 💬 1 📌 0

Retention subsidies are effective relative to other firm transfers b/c the data supports fairly elastic separations, and relatively inelastic vacancy creation.

16.01.2025 09:58 — 👍 1 🔁 0 💬 1 📌 0

UI duration extensions are effective relative to other household transfers b/c the data supports limited insurance with respect to long-term unemployment. At the margin, we can stimulate household consumption a lot by insuring them against this.

16.01.2025 09:58 — 👍 1 🔁 0 💬 1 📌 0

Untargeted transfers to households are, in general, quite ineffective, whereas targeted transfers to the unemployed, like UI duration extensions, and job-saving retention subsidies give a lot of bang for the buck.

16.01.2025 09:58 — 👍 2 🔁 2 💬 2 📌 0

We find that fiscal multipliers vary greatly across different common policy interventions, from 0.3 to 1.6. You cannot compare stimulus packages by just counting dollars spent, you must look under the hood at the actual design!

16.01.2025 09:58 — 👍 1 🔁 0 💬 1 📌 0

Quantitatively, we use a state-of-the-art calibration of the model, building on our previous work and that of Rohan Kekre.

www.dropbox.com/scl/fi/wf5fw...

sites.google.com/site/rohanke...

16.01.2025 09:58 — 👍 0 🔁 0 💬 1 📌 0

Intermezzo: Special thanks to @aauclert.bsky.social-Bardoczy-Rognlie-@ludwigstraub.bsky.social and Boppart-Krusell-Mitman for teaching us to think about models in sequence space.

16.01.2025 09:58 — 👍 0 🔁 0 💬 1 📌 0

We exploit these properties to investigate which parameters (and features of the model) are important for determining the relative effectiveness of a variety of different stimulus designs.

16.01.2025 09:58 — 👍 0 🔁 0 💬 1 📌 0

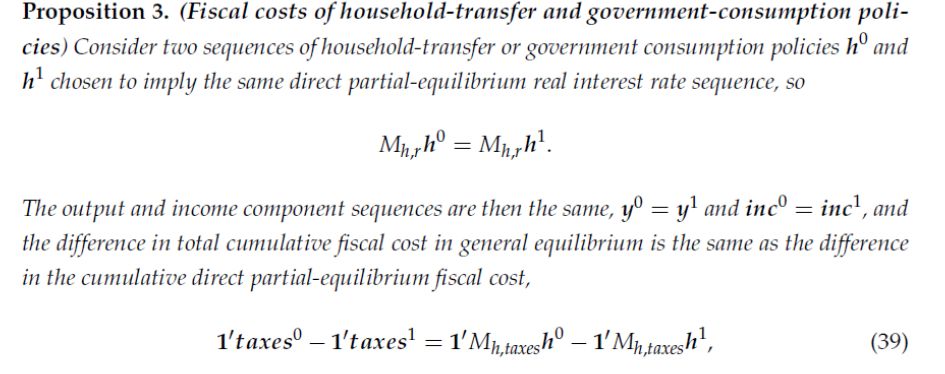

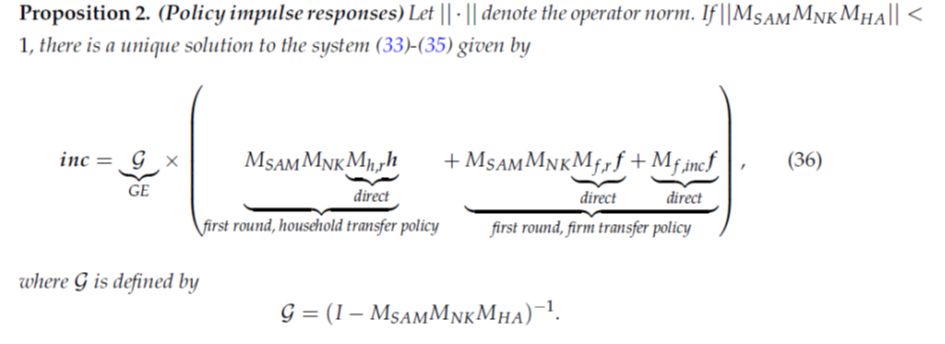

A direct implication is that for comparing the fiscal multipliers of two different policies that achieve the same output effect, in many cases we don’t need to know all the parameters of the model, but only the parameters relating to the policy-specific direct effect.

16.01.2025 09:58 — 👍 0 🔁 0 💬 1 📌 0

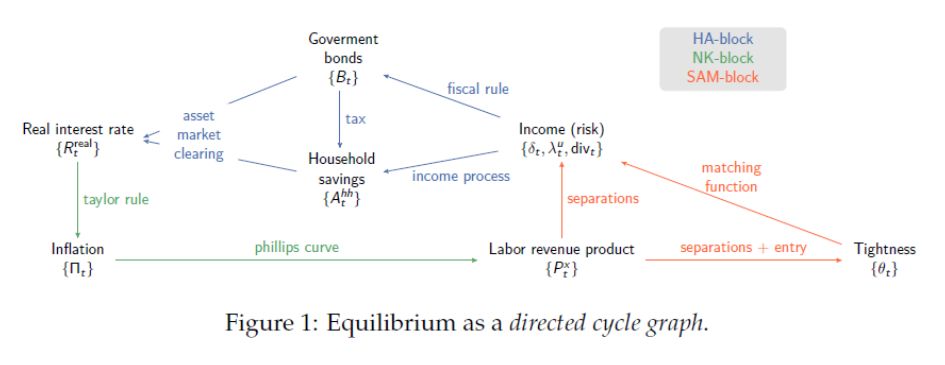

This means that a solution to any policy shock can be written as the product of a policy-specific direct effect, and a policy-invariant GE effect, where the latter is a geometric sum of repeated cycles through these three blocks.

16.01.2025 09:58 — 👍 0 🔁 0 💬 1 📌 0

An HA block determines the asset market equilibrium given the labor market equilibrium, an NK block determines the goods market equilibrium given the asset market equilibrium, and a SAM block determines the labor market equilibrium given the goods market equilibrium.

16.01.2025 09:58 — 👍 0 🔁 0 💬 1 📌 0

This is because a first-order approximation of the equilibrium in sequence space takes the form of a Directed Cycle Graph.

16.01.2025 09:58 — 👍 0 🔁 0 💬 1 📌 0

A key insight of our paper is that despite the model richness and its infinite-dimensional state space, we can nevertheless go quite far in characterizing this model analytically, especially when comparing the effect of different policy shocks.

16.01.2025 09:58 — 👍 1 🔁 0 💬 1 📌 0

Due to its richness, with realistic heterogeneity and frictions in several markets, the model is suitable for quantitatively comparing the effect of different policy designs. At the same time, the richness makes the comparison challenging.

16.01.2025 09:58 — 👍 1 🔁 0 💬 1 📌 0

Team Lead Economist at ECB’s Monetary Policy Strategy Team. From the cold North (#visitOulu). PhD from PSE. Tennis player, explorer

IFAU - Institutet för arbetsmarknads- och utbildningspolitisk utvärdering. Vi är ett statligt forskningsinstitut under Arbetsmarknadsdepartementet.

IFAU is a Swedish government research institute under the Ministry of Employment.

www.ifau.se

The official account of Stockholm University. Here, we publish research findings and other news from SU, as well as updates on when our researchers appear in the media or participate in public debates. Mainly in English.

su.se/english

su.se

The official feed of the Department of Economics at NHH - Norwegian School of Economics.

https://www.nhh.no/en/departments/economics/

Professor of Economics at Universität Hamburg

https://www.oposch.com

Assistant Professor in Economics, University of Minnesota. Development economics, macroeconomics, and a weekly rabbit hole.

Econ PhD Student at Uppsala/IFAU

Associate professor at Tufts University working in macro-labor, macro-climate, and international macroeconomics. Views are my own.

https://sites.google.com/view/alanfinkelsteinshapiro

Economics in Oslo/Scandinavia

karlharmenberg.com

Assistant Professor @Northwestern University working on macro, climate&energy, inequality and monetary policy

diegokaenzig.com

Policy-oriented macroeconomist. Visiting professor in economics at Uppsala University.

Macroeconomist studying labor. Senior economist at FRB. Opinions my own, RT \ne endorse. https://christopher-huckfeldt.github.io/

Econ AP University of Warwick, Ph.D. Brown University

https://www.saraspaziani.com/

Behavioral and development economist at MIT studying poverty, sleep, alcohol, mental health, and loneliness

Lecturer & Fellow in Economics at Trinity College, University of Cambridge. Research and writing on tax policy.

https://sites.google.com/view/kristofferberg/

Sociologist. Researcher at SOFI.su.se, Stockholm University

Research interests: Social capital, networks, beliefs in the future and Social class. Born 347 ppm.

Professor, Economics,

IIES - Stockholm University

https://sites.google.com/site/nilssonjanpeter/