NEW: How aggregate and idiosyncratic shocks affect household income dynamics.

📗 Read @manoloarellano.bsky.social, Martín Almuzara, @richardblundell.bsky.social and Stéphane Bonhomme's new cemmap working paper: ifs.org.uk/publications...

#econsky

12.08.2025 13:00 — 👍 8 🔁 5 💬 1 📌 0

YouTube video by Barcelona School of Economics

Keynote Speeches - Data Science & Specialized Economic Analysis - Graduation Ceremony 2025

Graduation speech at the Barcelona School of Economics

www.youtube.com/watch?v=jd4h...

27.08.2025 08:09 — 👍 4 🔁 1 💬 0 📌 0

Congratulations to Víctor Sancibrián for successfully defending his Ph.D. thesis at CEMFI!. Thanks to Aureo de Paula, Laura Hospido and Geert Mesters for serving in the Thesis Defense Committe and to Víctor’s advisor Manuel Arellano

25.06.2025 09:57 — 👍 12 🔁 3 💬 0 📌 0

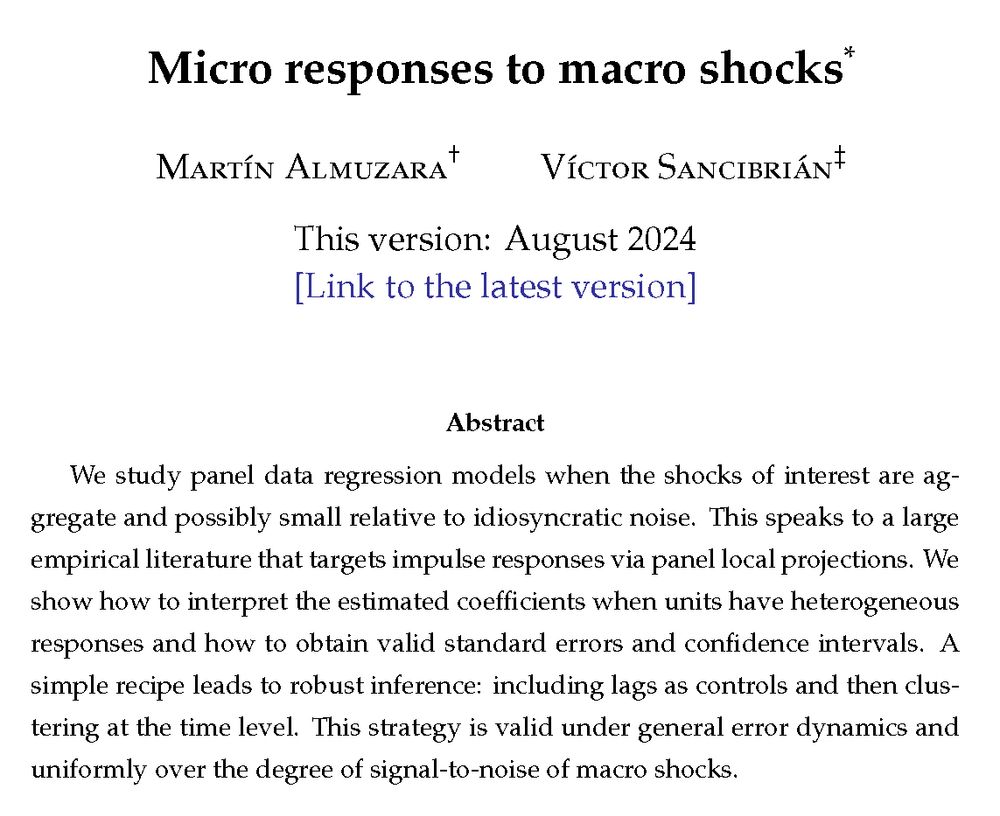

Working paper "Micro responses to macro shocks" by M. Almuzara and V. Sancibrián (Version August 2024).

Abstract: We study panel data regression models when the shocks of interest are aggregate and possibly small relative to idiosyncratic noise. This speaks to a large empirical literature that targets impulse responses via panel local projections. We show how to interpret the estimated coefficients when units have heterogeneous responses and how to obtain valid standard errors and confidence intervals. A simple recipe leads to robust inference: including lags as controls and then clustering at the time level. This strategy is valid under general error dynamics and uniformly over the degree of signal-to-noise of macro shocks.

Link: https://sancibrian-v.github.io/files/lp_panels.pdf

📢 We just posted a MATLAB suite for panel local projections.

It supports estimation and inference, including small-sample refinements, fixed-effects, controls, cumulative responses...

Available at github.com/TinchoAlmuza... together with replication files.

19.02.2025 18:11 — 👍 4 🔁 0 💬 0 📌 0

How should we think about estimation uncertainty of heterogeneous responses when the sample is a large fraction of the population?

Víctor Sancibrián explores this in repeated measurement problems, such as when documenting the extent of firm misallocation

sancibrian-v.github.io

14.11.2024 11:16 — 👍 7 🔁 3 💬 0 📌 1

What determines optimal deposit insurance coverage?

JMC Vedant Agarwal studies the effects of deposit insurance coverage on banks' exposure to runs, risk-taking incentives, fiscal costs, and welfare in a quantitative macroeconomic model with bank runs

vedant-agl.github.io

13.11.2024 11:26 — 👍 3 🔁 2 💬 0 📌 0

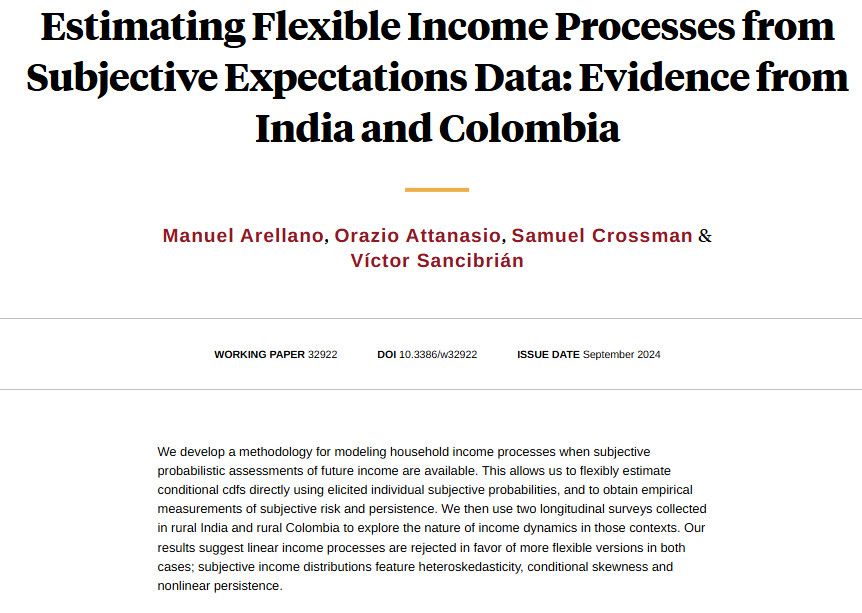

Developing a methodology for modeling household income processes when subjective probabilistic assessments of future income are available, from Manuel Arellano, Orazio Attanasio, Samuel Crossman, and Víctor Sancibrián https://www.nber.org/papers/w32922

14.09.2024 15:00 — 👍 5 🔁 3 💬 0 📌 1

Nonlinear persistence among the poorest households is consistent with a poverty trap interpretation: When income is too low it is difficult to escape poverty, but a large positive shock can weaken the weight of history and get the household (persistently) off the hook at a higher income level.

1/2

16.10.2024 08:21 — 👍 8 🔁 3 💬 0 📌 1

Researcher at CEMFI, transitioning to Universidad Autonoma de Madrid. Working on health, aging, gender, education, things a normal being would say are not econ.

https://sites.google.com/view/yarinefawaz/home

AP @unibocconi - previously @TPRI_BU in Boston and @mpi_inno_comp in Munich. All opinions my own. https://www.felixpoege.eu/

(Last name also as Pöge)

Assistant Professor of Economics at @uc3meconomics.bsky.social | PhD @cemfi.es | Political Economy and Economic Development.

https://www.daniela-sola.com

Macroeconomist | Assistant Professor @CEMFI

www.federicokochen.com

Applied Econometrician

Associate Professor at University of Oxford

Fellow and Tutor of Lady Margaret Hall

ditraglia.com

econometrics.blog

sqare.org

Assistant Professor of Econometrics at Uni Bonn

Interested in econometrics and statistics for a heterogeneous world

https://vladislav-morozov.github.io/

Econometrician. Professor of Economics and Professor of Statistics, Harvard University. Frank B. Baird Jr, Professor of Science

Associate Professor in Economics at the University of Geneva. Website: https://www.cgaillac.com/

Associate Professor (untenured) at Kobe University. Labor, Macro, and Family Economics

https://kazuyanagimoto.com

Economics Fellow at NYU Policy Integrity. I work on energy, environmental, and political economy issues using tools from empirical industrial organization. Basque.

https://pelloaspuru.github.io/

Economist. Now studying at @cemfi.es.

Research Economist at Banco de España (Views are my own) | Interested in macro, firm dynamics, productivity, monetary policy and finance | PhD in Economics from Uc3m | Alumni UAH | Website: https://beatrizgonzalezlopez.weebly.com

Assistant Professor at the University of Chicago. Economics Ph.D. from UC3M.

Political Economist. My soul was always for History.

Personal webpage: https://t.co/b9M6GHB6H5

Assistant Professor of Economics at Chicago Booth. @NYUniversity Econ PhD. I use IO tools to study the best human invention: cities.

Economics PhD student at LSE

Economics Professor at UC Berkeley; from #Ukraine

PhD candidate in Economics @UCL

Previously @CEMFI @PKU

Interested in economic development

First gen🎓

News from the editors of Econometrica

Research Economist at Banco de España | joelmarbet.com

PhD Candidate @Cemfi.es from 🇹🇷 | Labor and Gender | For more: sevinkaytan.com