thanks, Alex! we did not expect credit scores to matter as much, and I'm still pondering over the implications for housing affordability

15.04.2025 19:26 — 👍 0 🔁 0 💬 0 📌 0

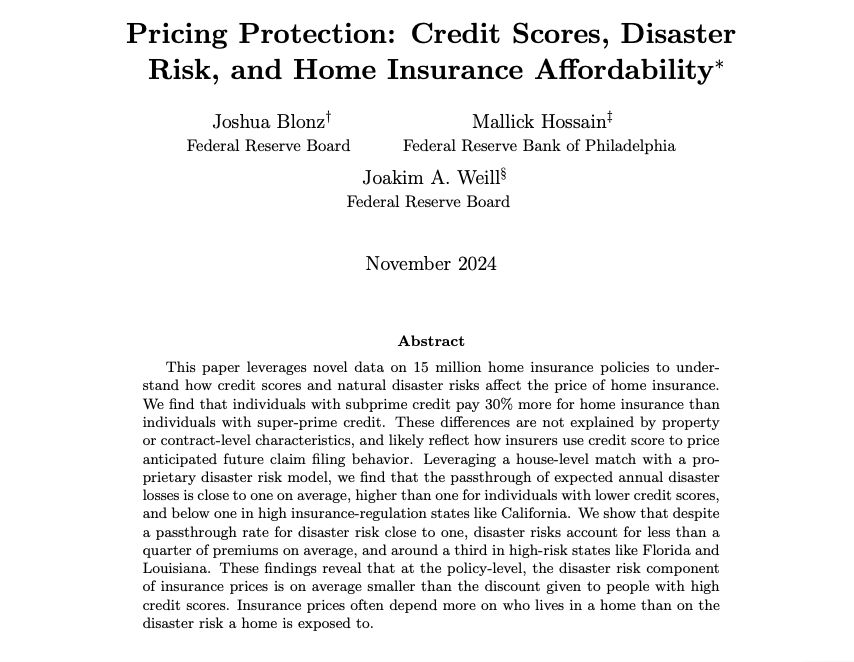

This paper leverages novel data on 15 million home insurance policies to understand how credit scores and natural disaster risks affect the price of home insurance. We find that individuals with subprime credit pay 30% more for home insurance than individuals with super-prime credit. These differences are not explained by property or contract-level characteristics, and likely reflect how insurers use credit score to price anticipated future claim filing behavior. Leveraging a house-level match with a proprietary disaster risk model, we find that the passthrough of expected annual disaster losses is close to one on average, higher than one for individuals with lower credit scores, and below one in high insurance-regulation states like California. We show that despite a passthrough rate for disaster risk close to one, disaster risks account for less than a quarter of premiums on average, and around a third in high-risk states like Florida and Louisiana. These findings reveal that at the policy-level, the disaster risk component of insurance prices is on average smaller than the discount given to people with high credit scores. Insurance prices often depend more on who lives in a home than on the disaster risk a home is exposed to

Important paper on the home insurance market. Authors use novel data on 15 million insurance policies + document many new descriptive facts.

For instance, "the average person’s homeowners insurance [costs] 17% of their monthly principal and interest payment."

papers.ssrn.com/sol3/papers....

14.04.2025 21:20 — 👍 18 🔁 3 💬 1 📌 0

whether the mandate (c) reduces adverse selection or causes market unraveling depends on the details of (a) and (b)

12.01.2025 16:13 — 👍 2 🔁 0 💬 0 📌 0

For b) we also need to specify what homes are covered by the public option (all homes? cf US flood insurance. only the riskiest homes? cf FAIR plans), BUT also the state involvement (full involvement like US flood insurance, or a backstop above given threshold like in France?)

12.01.2025 16:09 — 👍 1 🔁 0 💬 1 📌 0

What matters for (a) is rates regulation (what price are insurers allowed to charge?)

12.01.2025 16:09 — 👍 1 🔁 0 💬 1 📌 0

Economist @ Minneapolis Fed's Opportunity & Inclusive Growth Institute. There's a graph for that. Views are my own. (she/her) https://albrightalex.com/

Helping cities decarbonize at Bloomberg Associates. The rest of the time: urbanism, housing, running, trivia, baked goods, NYC.

Economist, Swedish University of Agricultural Sciences (SLU) @slu-econ.bsky.social. IntEcon/Env/Ag. Avid curler. Area editor, JAAEA.

Just ATE (Ag Trade Env) Blog: shonferguson.substack.com

Website: https://sites.google.com/view/shonferguson/home

Environmental economist, Professor @Cornell Brooks Public Policy, Fellow @Cornell Atkinson Center for Sustainability, President @aereorg.bsky.social. Views are my own.

https://sites.google.com/view/sheilaolmstead/

Climate economist, Columbia

https://gwagner.com

It’s pronounced juggernaut without the jug.

If I didn't bother writing it, you shouldn't have to bother reading it: https://gwagner.com/privacy

Associate Professor at ASU

#DevEcon #EnvironEcon #AgEcon #EnvironDemography #PoliticalEcon

Non-resident fellow at IFPRI

Member of AERE Org Board of Directors

Deputy Editor at Climatic Change

Environmental and health economist at @warwickecon

Cofondatrice di http://cblab.co

Capoerista.

@LudoGazze on #EconTwitter & econtwitter.net

Astenersi perditempo.

Economist with USDA-ERS | Food banks, food markets, and food security | PhD from Cornell, MS from Colorado State | Ithaca-based | Opinions are my own | Econanne.com

Professor and Head of Land Economics Group at Uni Bonn (@land-economics.bsky.social)

Website: https://www.ilr1.uni-bonn.de/en/research/research-groups/land-economics

Google Scholar: https://scholar.google.com/citations?user=3p-CJ1IAAAAJ&hl=de&oi=ao

An independent, nonprofit research institution dedicated to advancing a healthy environment 🌎 and thriving economy 📈 through impartial economic research and policy engagement.

https://www.rff.org/

Professor of Economics, Environmental Economist with interests in tropcial deforestation and development in the Brazilian Amazon

JEEM publishes theoretical and empirical papers addressing economic questions related to natural resources and the environment. Est. 1974.

https://www.sciencedirect.com/journal/journal-of-environmental-economics-and-management

Official BlueSky account of REEP, first published in 2007 and consistently ranked in the top-20 of all economics journals and top-15 of all environmental studies journals.

https://t.co/lW3lVRHOhr

As the official research journal of @aereorg.bsky.social, JAERE publishes papers that are devoted to environmental and natural resource issues.

https://www.journals.uchicago.edu/toc/jaere/current

Official BlueSky account of the Association of Environmental and Resource Economists.

Our journal posts are presented with #JAERE and #REEP.

resource economist | assistant professor at the University of Alberta