We are hosting the Canadian Macroeconomics Study Group at @westernu.ca!

This year's keynote is Kjetil Storesletten @hellerhurwicz.bsky.social

Program 👉 baxter-robinson.github.io/CMSG2025_Pro...

Registration is 100 CAD (70 for students!) 🔗https://economics.uwo.ca/about-us/workshops/index.html

23.09.2025 12:02 — 👍 8 🔁 4 💬 0 📌 0

The doors are always open here! Come back whenever you want!

19.07.2025 03:55 — 👍 1 🔁 0 💬 0 📌 0

Finally, it was fantastic to have an academic excuse to reconnect with friends that I haven't seen in a very long time 👋: David Echeverry, Cesar E. Tamayo, and Luis Felipe Saenz.

13.07.2025 16:58 — 👍 0 🔁 0 💬 0 📌 0

As part of the conference, we featured a full-day workshop on "Heterogenous Agents Models: A Toolkit for Policy Makers" jointly organized by Central Bank of Chile Research and CEMLA. A big thank you to Matias Ossandon Busch for his support.

13.07.2025 16:58 — 👍 0 🔁 0 💬 1 📌 0

Former graduate student Carlos Rondon Moreno and our colleague Christiane Baumeister catching up at a Central Bank of Chile conference:

09.07.2025 14:04 — 👍 1 🔁 2 💬 0 📌 0

The tragic landslide in Blatten gives me the excuse to tell you the story of how we found out Ice Ages existed. It's a cool story and the most important bit is rather similar to what's happening now.

29.05.2025 19:49 — 👍 956 🔁 416 💬 26 📌 97

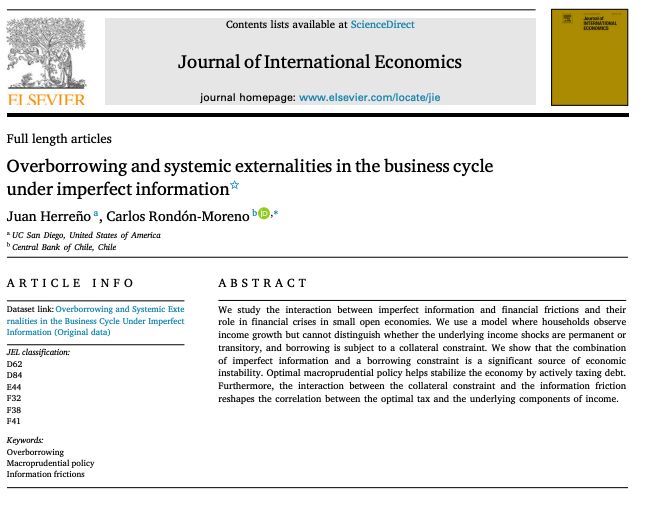

Proud of this work with @juanherreno.bsky.social. We believe these insights are critical for policymakers in emerging economies.You can find our paper in the Journal of International Economics, Vol 157.

Big thanks to my advisors at @ndecon.bsky.social!

📝 Link: shorturl.at/JdJhr

27.05.2025 23:22 — 👍 1 🔁 0 💬 0 📌 0

To sum up: Imperfect information about income shocks, when combined with borrowing constraints, is a potent source of economic instability. Optimal macroprudential policies are even more beneficial in this setting, and their design must account for these information frictions.

27.05.2025 23:22 — 👍 2 🔁 0 💬 1 📌 0

In our model, this shift occurs because uninformed households, fearing the non-tradable shock might signal a worse, permanent downturn, reduce borrowing anyway, even if their borrowing capacity technically increases. The planner then doesn't need to tax as aggressively

27.05.2025 23:22 — 👍 0 🔁 0 💬 1 📌 0

Our Figure 11 shows the shift in optimal tax policy for a temporary non-tradable income shock (Zᴺ). With perfect information (Panel a), the tax is procyclical; with imperfect information (Panel b), it becomes countercyclical (positive correlation with income).

Consider a temporary negative shock to "non-tradable" income:

🔹 With perfect info, the best policy is often to RAISE taxes as this income falls (procyclical).

🔹 With imperfect info, our model shows the optimal tax becomes COUNTERCYCLICAL – the planner reduces taxes as this non-tradable income falls!

27.05.2025 23:22 — 👍 1 🔁 0 💬 1 📌 0

However, one of the most fascinating results for us was how imperfect information alters the optimal tax response depending on the specific component of income that's hit by a shock. It's not a one-size-fits-all policy.

27.05.2025 23:22 — 👍 0 🔁 0 💬 1 📌 0

A really important result from our analysis: this imperfect information makes well-designed policy even more critical. We found the welfare gains from an optimal debt tax can more than double when agents can't perfectly distinguish shock types. The average optimal tax also tends to be higher.

27.05.2025 23:22 — 👍 0 🔁 0 💬 1 📌 0

How can policymakers address this? We analyze "macroprudential policy," specifically taxing foreign debt. A central planner, who can internalize the economy-wide effects that individual households might not, can use this tool to improve stability.

27.05.2025 23:22 — 👍 0 🔁 0 💬 1 📌 0

Figure 1 from our paper illustrates how agents' beliefs (dotted line) about income shocks can differ from the actual shocks (solid line) under imperfect information. For example, a permanent negative income growth shock (gₜ, bottom right) might be initially misperceived as less severe.

So why is this 'not knowing' the type of income shock so crucial in our model? Agents use available data (we model this with a Kalman filter) to guess. But their beliefs can diverge from reality!

27.05.2025 23:22 — 👍 0 🔁 0 💬 1 📌 0

What did we find? This combination – not quite knowing if good/bad times are permanent AND having borrowing limits – can significantly increase economic instability. It can lead to "overborrowing" and make financial crises more frequent.

27.05.2025 23:22 — 👍 0 🔁 1 💬 1 📌 0

Alongside this, we incorporate a common feature: how much households can borrow is limited by a "collateral constraint," often tied to their income.

27.05.2025 23:22 — 👍 0 🔁 0 💬 1 📌 0

We explore small open economies where households face a tricky situation. They see their income change, but it's hard to tell if it's a temporary blip or a long-lasting shift in their economic conditions. This is due to "imperfect information". #InformationFrictions

27.05.2025 23:22 — 👍 0 🔁 0 💬 1 📌 0

🚨 Excited to share insights from a paper I co-authored with @juanherreno.bsky.social on why emerging economies often face financial crises or "Sudden Stops"! Just published in Journal of International Economics (@jintlecon.bsky.social )

📝 Link: shorturl.at/JdJhr

#Econsky #Macroeconomics

27.05.2025 23:22 — 👍 12 🔁 6 💬 1 📌 0

#LaTeXTip: use the --aspectratio=169-- option to fit your #beamertex slide to most modern projectors (and screeens!): \documentclass[aspectratio=169]{beamer}

28.03.2025 01:07 — 👍 1 🔁 1 💬 0 📌 0

Great paper. Bequest motives, medical issues, wage risks and marriage/divorce are important drivers of lifetime wealth.

Also, great to see the joint work on one of our great former RAs at the Bank— @johanatch.bsky.social

20.03.2025 00:51 — 👍 0 🔁 0 💬 0 📌 0

Looking forward to today’s seminar by @mdenardi.bsky.social on “Savings and Labor Supply Over the Life Cycle” at the Central Bank of Chile. Live transmission available, don’t miss it! 🚨

#econSky @umn-econ.bsky.social

19.03.2025 11:31 — 👍 3 🔁 0 💬 1 📌 1

Excited to see @juanherreno.bsky.social at the Central Bank of Chile presenting his paper on the steepness of the Philips curve in distored economies.

#econsky #academicsky

12.03.2025 22:57 — 👍 8 🔁 0 💬 0 📌 0

Epic idea

11.03.2025 10:48 — 👍 42045 🔁 7189 💬 536 📌 323

Happy to see a nice summary of our paper on the March issue of @nber.org digest:

“The Unintended Consequences of Merit-Based Teacher Reform in Colombia.”

Can merit-based selection of public teachers necessarily leads to student’s learning gains?

Not always

#EconSky

www.nber.org/digest/20250...

04.03.2025 06:55 — 👍 6 🔁 2 💬 1 📌 1

Connected Documentation for Agile Teams 📄

Write, share, and collaborate in real time!

Learn more: https://hackmd.io/home

The world's third oldest professional football club.

Clwb pêl-droed proffesiynol trydydd hynaf y byd 🏴

noun | a reference source containing words alphabetically arranged along with information about their forms, pronunciations, functions, and etymologies

President, PIIE. Globalist. Former central banker. Political economy with a policy purpose. Writes on macroeconomic policy, G7/China relations, globalization, and economies of US, UK, Germany, Japan, and PRC.

European economics editor @TheEconomist. London via Berlin, Stockholm and Cologne. Have no plans to write a book.

— Founder of Our World in Data

— Professor at the University of Oxford

Data to understand global problems and research to make progress against them.

Economic Historian at Università di Torino. I aspire to a Plinian mind. From Palermo, Sicily.

Substack: https://andreamatranga.substack.com

Economist, interested in public economics, IO, and education. Fistball player and coach. From Llanquihue, Chile.

cristsanchez.github.io

Pronounced Kah-ren (かれん)

RA @ Bank

Formerly CS, Econ @ UCSD, SWE @ Intuit

ハーフ 🇺🇸🇯🇵

Nothing of substance occurs here

Personal account, views are my own

Economist, UT Austin, working on macro/monetary

www.oliverpfaeuti.com

Professor at Columbia Business School. Mostly international macro.

Professor of Economics, University of Oxford and Trinity College. https://sites.google.com/site/andreapferrero/home

Former NY Fed economist. Education: Bocconi/UPF/NYU. Originally from Italy. Also interested in sports, history and politics.

CESifo is a global, independent research network with members from across the world. Our mission is to advance international scientific knowledge exchange in economics and economic policy.

www.cesifo.org

The Journal of International Economics is intended to serve as the primary outlet for theoretical and empirical research in all areas of international economics

Economist. Ex Prof / central banker. Macro, politics, money, central banks, finance, Brexit, covid, AI, climbing, MUFC, Blueskyism.

I was an academic economist for over 10 yrs (UMinn, TrinityU, UChicago) now I work as a researcher specializing in macro-system impacts of digital assets, money, & payments (crypto/stablecoins/CBDCs). #EconSky #Chicago

www.digitaleconomyconsulting.com

Doting grandmother, among other things.

Senior Economist @European Central Bank, Monetary Policy Directorate

Co-author of How Global Currencies Work (Princeton University Press)

Co-founder of www.globalcurrenciesdatabase.com

https://www.linkedin.com/in/livia-chitu-019772306/

Views are my own

Prime Minister of Canada and Leader of the Liberal Party | Premier ministre du Canada et chef du Parti libéral

markcarney.ca