We discuss it some more here www.financialresearch.gov/briefs/files...

04.03.2025 20:27 — 👍 3 🔁 0 💬 1 📌 0

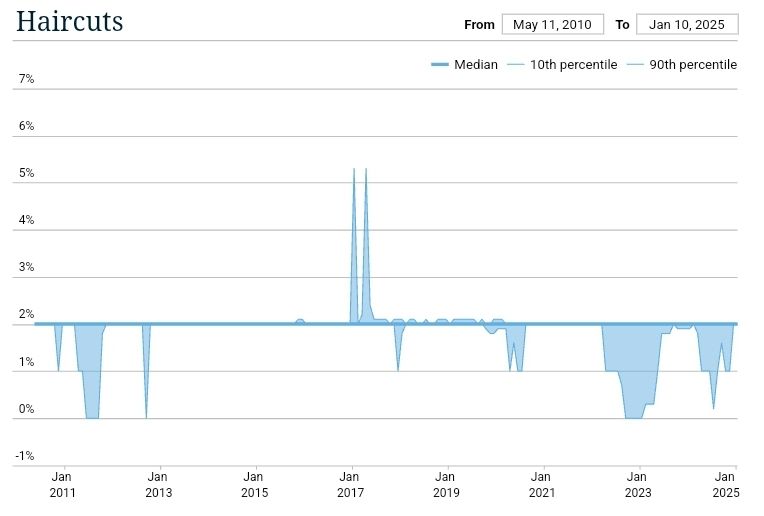

Even with these reasons in hand, that triparty haircuts are so uniformly at or near 2% regardless of market conditions suggests this may be a useful convention for traders trying to pack a lot of transactions into very little time, rather than carefully calibrated protection.

18.02.2025 14:32 — 👍 0 🔁 0 💬 1 📌 0

Reason 3: Many tri-party lenders are money market funds bound by 2a-7.

They are allowed to treat repo as an investment in the underlying security only if it is "collateralized fully," which may be interpreted as requiring a strictly positive haircut under the definition below.

18.02.2025 14:32 — 👍 0 🔁 0 💬 1 📌 0

Reason 2: Triparty is a general collateral market meaning that dealers have an incentive to use their worst collateral. So they aren't concerned about losing collateral.

Bilateral is specific collateral and may be used to source securities the borrower doesn't want to lose.

18.02.2025 14:32 — 👍 0 🔁 0 💬 1 📌 0

Meanwhile, bilateral features a lot of both borrowing and lending by hedge funds to dealers, so sometimes it may be the dealer-borrower who need protection rather than the lender.

www.financialresearch.gov/briefs/files...

18.02.2025 14:32 — 👍 0 🔁 0 💬 1 📌 0

Three big reasons for the gap:

Reason 1: Counterparty risk in triparty is generally lower—triparty is mostly safe banks and money market funds lending to riskier dealers—so lenders generally demand protection.

www.federalreserve.gov/econres/note...

18.02.2025 14:32 — 👍 0 🔁 0 💬 1 📌 0

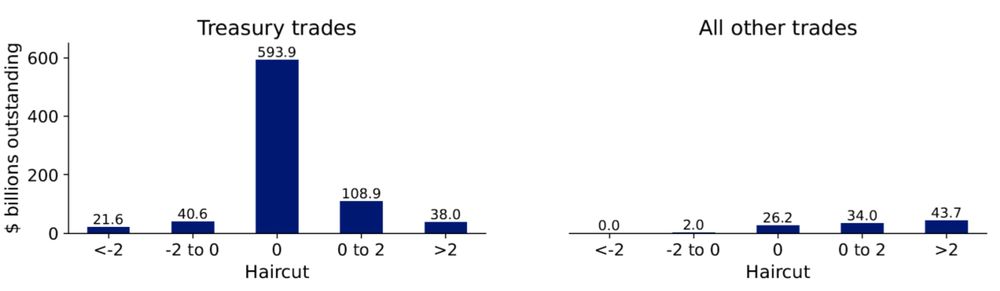

2% haircuts have become a fixation for many thinking about hypothetical minimum margins.

Since we've had the triparty data for a long time, people have gotten used to thinking 2% was "correct," but as we point out in the note triparty is a very different market from bilateral.

18.02.2025 14:32 — 👍 0 🔁 0 💬 1 📌 0

In non-centrally cleared bilateral repo, 70% of haircuts are zero, while triparty repo almost always applies a 2% haircut, giving the lender substantially more protection.

Why is there such a big gap?

18.02.2025 14:32 — 👍 1 🔁 1 💬 1 📌 1

We also argue that cross-margining should be applied where practicable, for instance in cash-futures basis trades.

While cross-margining may allow greater leverage, it also reduces risk of firesales if volatility increases by accounting for correlations between cash and futures

14.02.2025 15:03 — 👍 0 🔁 0 💬 0 📌 0

More generally, proportionate margins reflect the full set of risks of exposures and collateral surrounding a transaction.

To the extent exposures offset, as for correlated collateral in a "netted package," that should be reflected in margin collected.

14.02.2025 15:03 — 👍 0 🔁 0 💬 1 📌 0

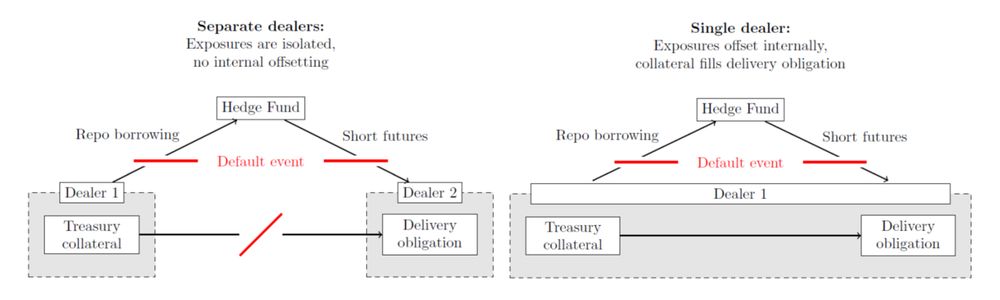

Our previous research showed that in this case, haircuts are often negative, to provide the dealer with protection against the hedge fund.

A consistent minimum haircut would undo this protection, since it would instead require a payment 𝘧𝘳𝘰𝘮 the dealer 𝘵𝘰 the hedge fund.

14.02.2025 15:03 — 👍 0 🔁 0 💬 1 📌 0

For example, sometimes hedge funds will source a specific Treasury by lending against it to a dealer.

In this case, even though the hedge fund is the lender, the dealer is the one who needs a cushion to protect against losing a valuable security to the hedge fund's default.

14.02.2025 15:03 — 👍 0 🔁 0 💬 1 📌 0

Instead, proportionate margins should:

1) Protect all participants in a transaction (not just one side),

2) Reflect both counterparty and collateral risk,

3) Account for the full portfolio of exposures between counterparties.

Minimum haircuts don't satisfy these properties.

14.02.2025 15:03 — 👍 0 🔁 0 💬 1 📌 0

Recent research by my coauthors and me finds that over 70% of haircuts in non-centrally cleared bilateral repo are zero, leaving no cushion for lenders.

www.financialresearch.gov/briefs/files...

This has, in turn, sparked interest in mandatory minimum haircuts in repo.

14.02.2025 15:03 — 👍 0 🔁 0 💬 1 📌 0

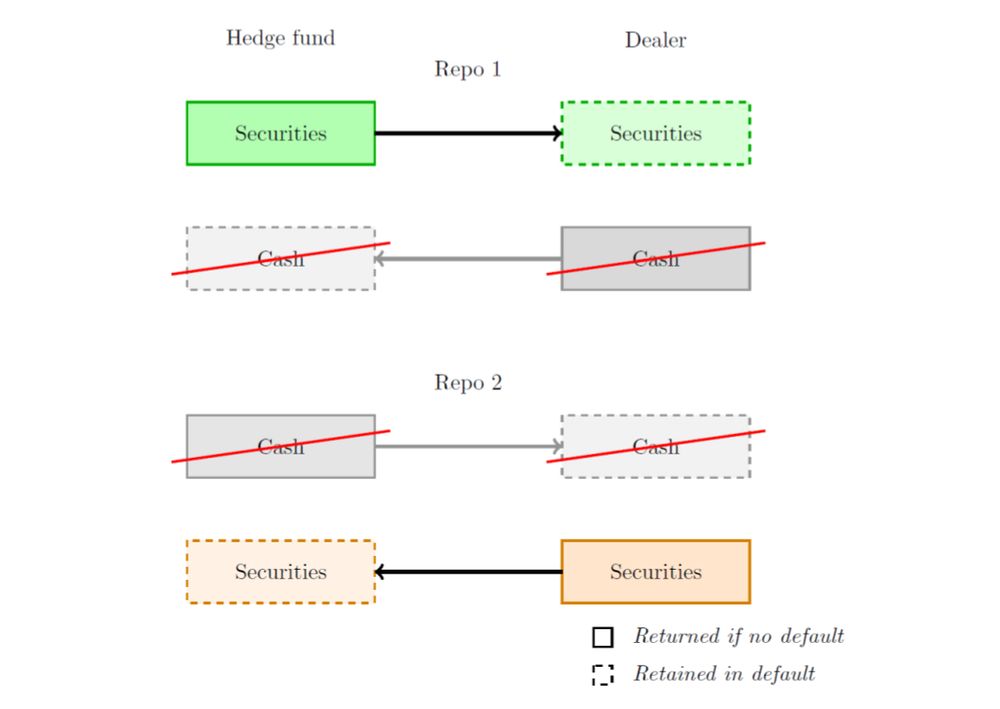

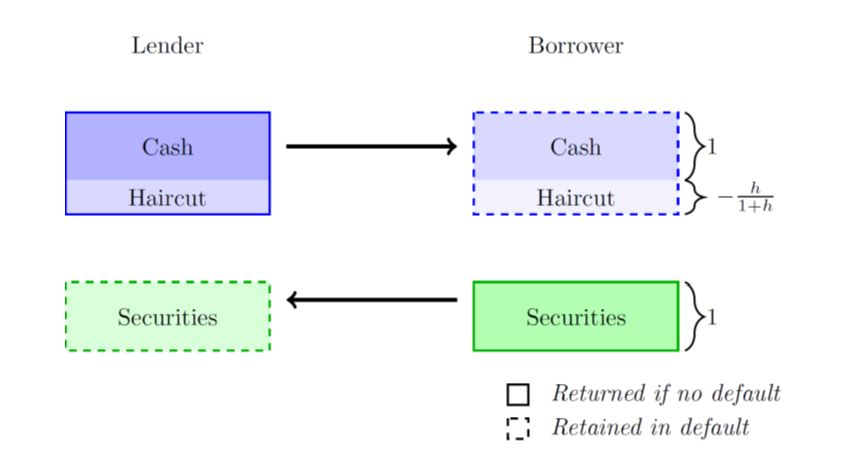

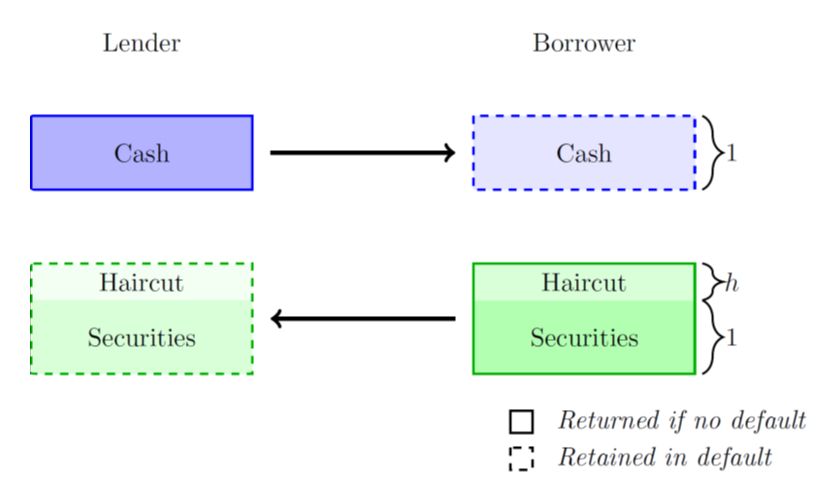

A positive haircut provides a cushion if the borrower defaults, helping the lender recover losses even if the collateral’s value dips or proves costly to liquidate.

14.02.2025 15:03 — 👍 0 🔁 0 💬 1 📌 0

Outside of clearing, repo margining is determined by "haircuts": a degree of overcollateralization that guards against default risk.

For instance, if you lend $100 and require $102 of collateral, the haircut is 2%.

14.02.2025 15:03 — 👍 1 🔁 0 💬 1 📌 0

Recently, there’s been growing concern about low or zero haircuts in repo markets.

In a new note, we argue that safety and liquidity can both be enhanced by setting repo margins that are 𝘱𝘳𝘰𝘱𝘰𝘳𝘵𝘪𝘰𝘯𝘢𝘵𝘦 to each counterparty’s actual risk.

www.federalreserve.gov/econres/note...

Thread below:

14.02.2025 15:03 — 👍 3 🔁 1 💬 1 📌 1

Just released: Update using N-PORT data running through 2024 Q4, live at j-kahn.com/nport/.

11.02.2025 17:19 — 👍 1 🔁 0 💬 0 📌 0

I can tell I'm getting old because when I google one of my favorite bands from high school, it sends me to 'warning signs for Strokes.'

25.11.2024 01:23 — 👍 1 🔁 0 💬 0 📌 0

In the counterfactual, Tyler is stuck behind me in his car as I take up the *full lane* on my bike.

22.11.2024 00:22 — 👍 0 🔁 0 💬 0 📌 0

Going forward I'll be updating this data on a quarterly basis, adding new series and improving the data quality as I go. Any comments or questions are welcome!

17.11.2024 19:13 — 👍 0 🔁 0 💬 0 📌 0

This data was compiled for our paper on mutual funds' use of Treasury futures: papers.ssrn.com/sol3/papers....

It's totally free, but we ask that if you use the data you cite the working paper

17.11.2024 19:13 — 👍 0 🔁 0 💬 1 📌 0

Excited to share our N-PORT data release is now live at j-kahn.com/nport/. Over 200K filings from mutual funds, ETFs & more since 2019 Q4.

This preliminary data has fund-level detail on portfolio allocations, maturities, notional derivatives, Treasury futures, and more!

17.11.2024 19:13 — 👍 0 🔁 0 💬 1 📌 1

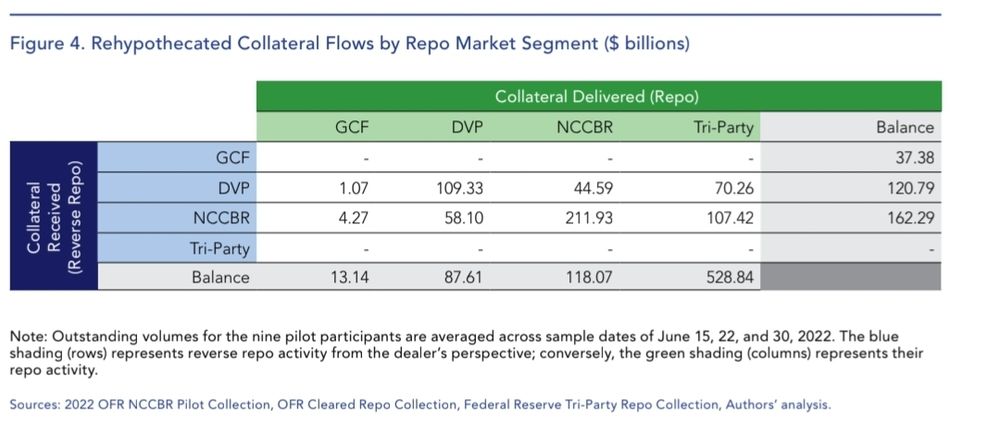

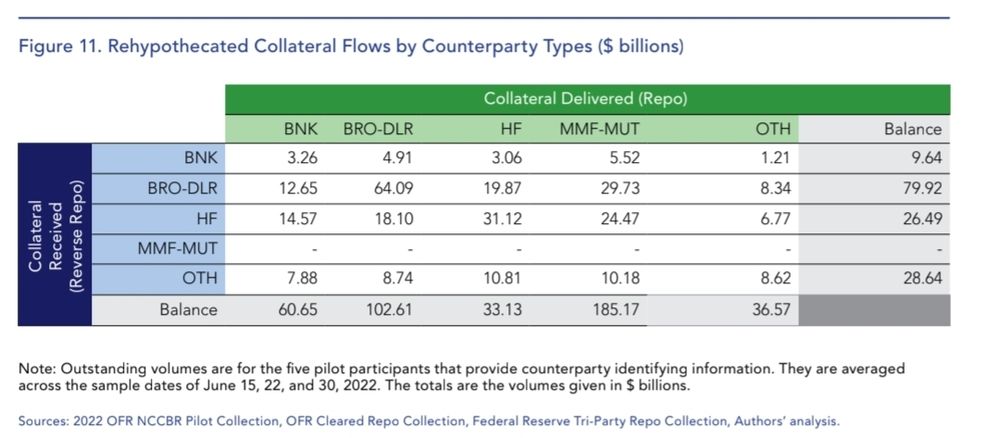

Tracking the flow of collateral across markets allows us to see useful patterns such as the that most tri-party collateral is not sourced from other repo markets (since valuable collateral will be locked up) but bilateral markets are more likely to circulate and reuse collateral.

14.11.2024 17:20 — 👍 0 🔁 0 💬 0 📌 0

We find that dealers rehypothecate about 65% of the collateral they receive, but face a variety of risks in intermediating these flows.

(all credit to Mark and Robert for this novel way of organizing the data which brings out the transfer)

14.11.2024 17:20 — 👍 0 🔁 0 💬 1 📌 0

New brief out with Sam Hempel, @markpaddrik and Robert Mann using comprehensive data across all four segments of the U.S. repo market to track collateral flows and repo intermediation.

www.financialresearch.gov/briefs/files...

14.11.2024 17:20 — 👍 0 🔁 0 💬 1 📌 0

Housing, money markets, financial stability. Just a guy at a regional office of a very large fixed income portfolio manager.

monetary economics|history of money|central banking|financial privacy|payments|gold|financial inclusion|cryptocurrency|monetary law|financial crime

I write at www.moneyness.ca

Economic history (mostly monetary and fiscal, various places and centuries)

Economist at the Federal Reserve Bank of Chicago (usual disclaimer applies)

Economist. Ex Prof / central banker. Macro, politics, money, central banks, finance, Brexit, covid, AI, climbing, MUFC, Blueskyism. More analysis later.

Historian of economics. Interested in macro and monetary economics, the role of economics as expert knowledge in central banks, and the history of economics in Colombia.

https://jcaacostamacia.github.io/Website/index.html

Macroeconomist from western Colorado. Views are my own.

https://rdecker.net

Follow me if you like having your deep-seated beliefs about monetary and banking history and policy challenged. And help me by challenging mine in turn!

Will talk science, tech, economics, politics

Mainly post stupid puns and captions for pictures

Cares about inequalities and exclusion, particularly around health

Enjoys cricket

FT Alphaville reporter. Ex-“veteran” fund manager. Resolution Foundation Assoc. Baring Foundation Trustee.

Executive Board of the European Central Bank, University of Bonn (on leave) #NieWiederIstJetzt

Climate / energy / materials / climate dad / Sneaky Sasquatch / in 🇸🇬. Posts are on rolling delete.

syncretica.substack.com

https://scholar.google.com/citations?user=1Vg7PNIAAAAJ&hl=en

Finance Professor at the University of Chicago Booth School of Business.

Economist at the New York Fed. Studies climate risk, real estate and corporate finance, UT Austin PhD. Views my own and not the Fed. He/him

Economist at San Francisco Fed. Macro-finance, monetary policy, climate finance. Husband and proud dad of two. From Hamburg (Moin!)

Associate Professor of Finance

Simon Graduate School of Business

University of Rochester

https://sites.google.com/view/alanmoreira/

Financial crises & how to fight them. steven.kelly@yale.edu

Substacking on financial stability topics at www.withoutwarningresearch.com (free)

Financial economist

www.rudigerweber.com

I'm a finance professor at the University of Georgia. https://www.malcolmwardlaw.info/

Banking and Corporate Finance, Labor, Statistical Methods

Dune is about worms.

Associate Professor of Finance. University of Oregon. https://robertready.github.io/research/